How Your Credit Score Is Calculated, Factor by Factor

Your credit score decides what you pay for a mortgage, a car loan, sometimes even car insurance, yet the formula behind it feels like a black box. It isn't. The weights are published, the levers are knowable, and once you see them, improving your score stops being guesswork.

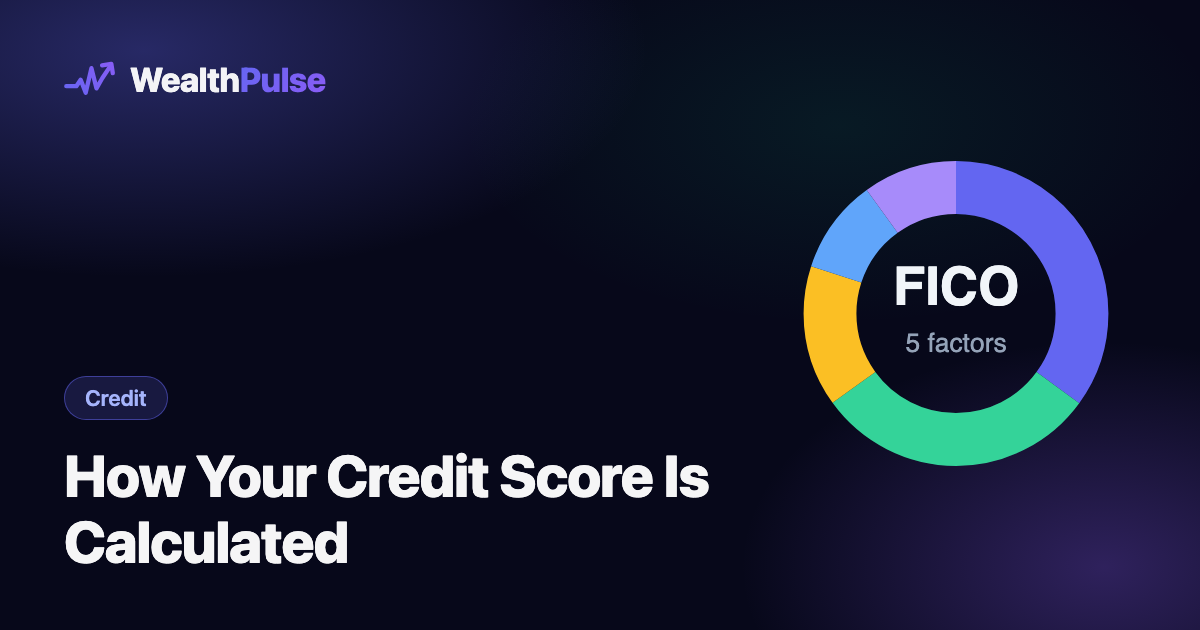

What goes into a credit score?

A FICO credit score is calculated from five factors: payment history (35%), amounts owed or credit utilization (30%), length of credit history (15%), credit mix (10%), and new credit (10%). The score ranges from 300 to 850 and is built entirely from the information in your credit reports at Equifax, Experian, and TransUnion.

Two things are worth knowing before we go factor by factor. First, roughly 90% of top lenders use FICO scores, so that's the model this guide follows (we'll cover how VantageScore (the number most free apps show you) differs below). Second, the weights are averages: if your credit history is short, the model leans harder on the data it has, so the same action can move two people's scores by different amounts.

Factor 1: Payment history: 35%

The single biggest question a lender has is simple: do you pay back what you borrow, on time? Payment history answers it, which is why it carries more weight than any other factor. FICO looks at the frequency, recency, and severity of missed payments across credit cards, installment loans, mortgages, auto loans, and student loans.

The numbers here are brutal and worth internalizing. A single payment reported 30+ days late can knock 60–110 points off a good score, and the damage escalates at 60 and 90 days. The flip side: recency matters. A late payment from three years ago counts far less than one from three months ago, so the account starts healing the moment you get back on track, though the mark itself can linger on your report for up to seven years.

How to win this factor: automate at least the minimum payment on every account. Perfection is the whole game here: there's no partial credit for "mostly on time." If you're juggling several due dates, a subscription and bill tracker that shows every recurring charge in one place removes the "I forgot" failure mode entirely.

Factor 2: Amounts owed (credit utilization): 30%

Utilization is the share of your available credit you're actually using. A $3,000 balance on $10,000 of limits is 30% utilization. FICO reads high utilization as a sign you're stretched: statistically, people who run their cards near the limit default more often.

Here's where most advice is subtly wrong. "Keep it under 30%" is repeated everywhere, but 30% is closer to a danger threshold than a goal. People with 800+ scores typically use well under 10% of their credit. FICO's own data on top scorers shows average utilization around 6%. And it's measured both per-card and overall, so one maxed-out card hurts even if your total is low.

Utilization is also your fastest lever, because it has no memory: the score only looks at the balances currently being reported. Pay a card down this month and the benefit shows up as soon as the new balance posts, usually within 30–45 days.

How to win this factor: pay balances down before the statement closes (that's usually the number reported), ask for credit-limit increases on cards you already handle well, and never close an old card just because you paid it off: the open limit is doing quiet work for your ratio.

Factor 3: Length of credit history: 15%

This factor looks at the age of your oldest account, your newest account, and the average age of everything in between. Longer is better because more history means more evidence. FICO has noted that the highest scorers opened their first account around 25 years ago, with an average account age of about 11 years.

You can't rush time, but you can avoid resetting the clock. Closing your oldest card eventually shrinks your average age; opening several new accounts at once drags it down immediately.

How to win this factor: keep your oldest no-fee card open (put one small recurring charge on it so the issuer doesn't close it for inactivity), and be patient. This is the factor that rewards simply not messing up.

Factor 4: Credit mix: 10%

Lenders like evidence you can handle both revolving credit (credit cards, lines of credit) and installment credit (auto loans, mortgages, student loans). Managing the two well signals broader competence than one alone.

At 10%, though, this is a minor factor, and it is not a reason to borrow money you don't need. Taking out a loan purely to diversify your mix costs real interest to chase a handful of points.

How to win this factor: let it happen naturally. If you have loans, pay them well; if you only have cards, don't manufacture debt. The mix improves on its own as your financial life unfolds.

Factor 5: New credit: 10%

Every time you apply for credit, the lender does a hard inquiry on your report. One inquiry typically costs a few points, usually in the 3–10 range, and fades within a year. The real risk is clustering: several applications in a short window reads as financial distress, especially on a young file.

Two important carve-outs. Checking your own score is a soft inquiry and never hurts you. And rate-shopping for the same loan type (say, a mortgage or auto loan) within a short window is typically treated as a single inquiry, so comparing lenders won't bury you in point deductions.

How to win this factor: apply for credit when you need it, not whenever a sign-up bonus winks at you, and go quiet on applications for six months before a major loan like a mortgage.

What the ranges mean, and where you stand

The national average FICO score is 715, solidly "good," though it slipped from 717 recently, driven partly by student-loan delinquencies returning to credit reports after the pandemic-era pause. But the tier label matters less than the pricing cutoffs lenders actually use: around 760+, you generally qualify for the best rates available, and pushing from 760 to 820 buys you nothing more. The gap below is where the money is: the difference between a ~620 and a ~760 score on a 30-year mortgage can be tens of thousands of dollars in extra interest.

FICO vs. VantageScore: why your app shows a different number

Credit Karma and most free tools show VantageScore, built by the three bureaus. It uses the same 300–850 scale and mostly the same data, but weighs it differently, and it can score you with as little as one month of history, where FICO needs six. Neither is "wrong"; they're two graders reading the same transcript.

| What's measured | FICO weight | VantageScore (approx.) |

|---|---|---|

| Payment history | 35% | 41% |

| Utilization / amounts owed | 30% | 20% utilization + 6% balances + 2% available credit |

| History length & mix | 15% + 10% | 20% "depth of credit" (combined) |

| New / recent credit | 10% | 11% |

The practical takeaway: don't panic when two apps disagree by 15 points. Track the trend in one score rather than the gap between two.

What your score does not include

Your income, savings, job title, and net worth are nowhere in the formula: a high earner can have terrible credit and vice versa. And by law (the Equal Credit Opportunity Act), race, religion, national origin, sex, marital status, and age can't be used in credit scoring. The score measures one thing: how you've handled borrowed money.

How to actually use your credit score

Knowing the formula is step one. Using it strategically is where the payoff lives:

Sequence your improvements by speed. Utilization moves in weeks, payment history heals in months, account age builds in years. If a mortgage application is six months out, attack card balances now. That's the lever that can still move in time.

Time your big applications. Check your score months before a major loan, not the week of. Pause new credit applications in the run-up, and pay cards down before statements close so the reported balances are low when the lender pulls your file.

Check your reports for errors. They're common. You can pull your full reports free every week at AnnualCreditReport.com. Creditors must be able to verify what they report; if something's wrong, dispute it with the bureau. This is one of the few genuinely free score boosts available.

Watch the score in context, not isolation. Your score interacts with everything else: the debt driving your utilization is the same debt in your payoff plan, and the payments protecting your history come out of your monthly budget. Tracking them together is the point of a dashboard like WealthPulse, where your debt payoff plan (avalanche or snowball, with your payoff date and interest saved) sits next to your budget and net worth, so a score strategy is never fighting your cash-flow reality.

See the whole picture behind your score. WealthPulse puts your debts, payoff plan, subscriptions, and budget in one dashboard, so the balances that drive your utilization and the due dates that protect your payment history are impossible to lose track of.

Frequently asked questions

What are the 5 factors of a credit score?

FICO scores are calculated from five factors: payment history (35%), amounts owed / credit utilization (30%), length of credit history (15%), credit mix (10%), and new credit (10%). Payment history and utilization together make up almost two-thirds of your score.

Does checking my own credit score lower it?

No. Checking your own score is a soft inquiry, which never affects your credit. Only hard inquiries (when a lender pulls your report because you applied for credit) can lower your score, and typically only by a few points.

What is a good credit utilization ratio?

Below 30% is the commonly cited threshold, but that's closer to a danger line than a target. People with the highest scores typically use well under 10% of their available credit, often in the single digits. Lower is better, both overall and on each individual card.

How much does one late payment hurt your credit score?

A payment reported 30+ days late can drop a good score by 60–110 points, and the damage grows at 60 and 90 days. The impact fades over time as long as you pay on time afterward, but the mark can stay on your report for up to seven years.

Why is my credit score different on different apps?

You have many scores, not one. Free apps usually show VantageScore, while most lenders use FICO, and each of the three bureaus (Equifax, Experian, TransUnion) may have slightly different data on you. The numbers should be close, but they're rarely identical.

How fast can you raise your credit score?

Utilization is the fastest lever: paying down card balances can move your score within one or two reporting cycles (30–60 days), because utilization has no memory. Payment history and account age, by contrast, only improve gradually over months and years.

The bottom line

Your credit score isn't a mystery and it isn't a judgment of your worth: it's five weighted measurements of how you handle borrowed money. Two of them (payments and utilization) are nearly two-thirds of the whole game and are fully in your control this month. One (account age) rewards patience. The other two mostly reward leaving things alone. Pay on time, keep balances low, protect your oldest accounts, apply sparingly, and let the math work for you instead of against you. And once the score is working for you, point the same discipline at the bigger goal: here's how much you really need to retire.

This article is general educational information, not financial advice. All analysis is for informational purposes only. Score impacts vary by individual credit profile. For guidance specific to your situation, consider speaking with a qualified financial professional.

Take control of your money

Budgeting, investing, and AI analysis in one dashboard. 7-day free trial.

Start free trial →