The 50/30/20 Rule: When It Breaks Down and How to Use It

If budgeting makes your eyes glaze over, the 50/30/20 rule is probably the friendliest place to start. There are no spreadsheets with forty categories, no apps pinging you about a $4 coffee. Just three buckets and one easy-to-remember split.

But here's the part most articles skip: the rule isn't a law of nature. For a lot of people, in a lot of situations, it quietly falls apart. The good news is that understanding why it breaks is exactly what turns it from a rigid formula into a tool you can actually use.

What the 50/30/20 rule actually says

The idea comes from All Your Worth: The Ultimate Lifetime Money Plan, a 2005 book by Elizabeth Warren and her daughter Amelia Warren Tyagi. You take your after-tax income and divide it three ways:

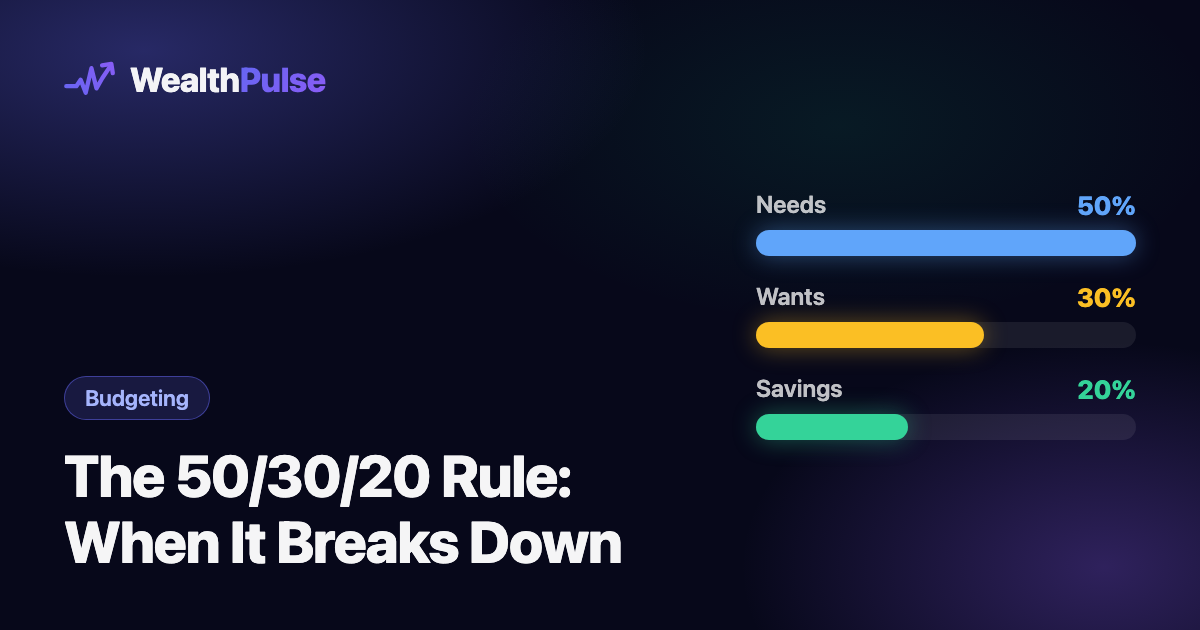

- 50% to needs: rent or mortgage, groceries, utilities, insurance, minimum debt payments, transportation to work. The stuff you genuinely can't skip.

- 30% to wants: dining out, streaming, hobbies, travel, the nicer brand of everything. Things that make life enjoyable but wouldn't sink you if they disappeared.

- 20% to savings and debt payoff: emergency fund, retirement, investments, and any extra you throw at debt beyond the minimums. That 20% is what makes your net worth statement move month over month.

The whole appeal is the simplicity. You don't track every transaction; you just keep three rough proportions in check. For someone who's never budgeted before, that's a genuine breakthrough.

Why it's so popular

A budget only works if you actually follow it, and most detailed budgets fail because they ask too much. The 50/30/20 rule survives contact with real life because it's forgiving. Spend a little more on wants one month and a little less the next? Fine. The buckets are big enough to absorb normal messiness, which means people stick with it long enough to build real habits.

It also reframes saving as non-negotiable. By carving out that 20% as its own category, the rule treats your future self as a bill that has to get paid, not as whatever happens to be left over (which, for most people, is nothing).

When the rule breaks down

Here's where the honesty comes in. The 50/30/20 split assumes a fairly specific situation: a middle income, a manageable cost of living, and not too much debt. Move away from that center and the math stops cooperating.

When your cost of living is high. In expensive cities, rent alone can eat 40–50% of take-home pay before you've bought a single grocery. Stuff needs into 50% and you're not overspending. The housing market is just bigger than the rule allows. The percentages were never adjusted for a one-bedroom that costs $2,500 a month.

When your income is low. At lower incomes, needs don't scale down the same way wants do. Rent, food, and utilities have a floor. If essentials swallow 70% of your paycheck, the problem isn't discipline. It's that there's no "30% for fun" hiding anywhere. Telling someone in this spot to "just follow 50/30/20" can feel out of touch.

When your income is high. The opposite problem. If you earn a lot, you may not need 50% for needs or want to spend 30% on wants, and saving only 20% might leave a lot of future wealth on the table. Lifestyle inflation loves to fill that 30% bucket. High earners often do far better aiming for a 30–40% savings rate.

When your income is irregular. Freelancers, gig workers, commission earners, and small business owners don't have a steady "after-tax monthly income" to slice up. A great month and a terrible month average out to numbers that describe neither. Fixed percentages struggle when the denominator keeps moving.

When you're carrying heavy debt. High-interest debt (think credit cards at 20%+ APR) doesn't fit neatly. The minimum payment counts as a "need," but the smart financial move is usually to attack it aggressively, which means borrowing from the wants bucket and possibly the savings bucket too. The rule's tidy 20% can't keep up with the urgency.

The needs-vs-wants problem. Is a car a need? What about your phone? A gym membership for your health? The line between needs and wants is genuinely blurry, and most of us are very good at relabeling a want as a need when it's convenient. Two honest people can sort the same expenses completely differently.

How to actually use it well

None of this means you should toss the rule out. It means you should treat it as a starting compass, not a finish line. Here's how to make it work for your real life.

Track one honest month first. Before you assign percentages, find out where your money already goes. Most people are surprised, and you can't adjust ratios that don't match reality.

Adjust the ratios to fit you. The framework is the gift, not the specific numbers. Try the variation that matches your situation:

- High cost of living: 60/20/20 or 70/20/10

- Aggressive saver or high earner: 50/20/30 or 40/20/40

- Paying down high-interest debt: shrink wants temporarily and pour it into payoff

Pay yourself first. Automate the savings transfer for the day you get paid, before the money has a chance to evaporate. When saving happens automatically, you budget what's left instead of saving what's left. (Where should that 20% ultimately point? See how much you really need to retire.)

For irregular income, budget on a baseline. Build your plan around your lowest typical month. In strong months, route the surplus straight to savings or debt instead of upgrading your lifestyle to match the peak.

Revisit it at every life change. A raise, a move, a new kid, a paid-off loan: each one shifts the math. The ratios that fit you at 25 won't fit at 40, and that's normal.

A quick example

Say you bring home $4,000 a month after taxes. The textbook split is $2,000 needs, $1,200 wants, $800 savings. But your rent runs $1,800 and your essentials total $2,400, already 60% of your income.

Instead of pretending you're overspending, you adjust: 60% needs, 20% wants ($800), 20% savings ($800). Same framework, honest numbers. You've kept the discipline of an automatic savings bucket while accepting the reality of your rent. That's using the rule well.

Try it with your own numbers

The bottom line

The 50/30/20 rule is one of the best on-ramps to budgeting ever invented: simple enough to remember, forgiving enough to follow. Just don't mistake it for a verdict on whether you're doing money "right." Your numbers depend on your income, your city, and your debt, and the smartest budgeters bend the ratios to fit their lives rather than bending their lives to fit the ratios.

Start with the framework. Keep the habit of paying your future self first. Adjust everything else.

This article is general educational information, not personalized financial advice. For guidance specific to your situation, consider speaking with a qualified financial professional.

Take control of your money

Budgeting, investing, and AI analysis in one dashboard. 7-day free trial.

Start free trial →