How to Read a Net Worth Statement (and Track Yours)

Your bank balance tells you what you can spend this week. Your salary tells you what flows in. Neither tells you whether you're actually building wealth. That's the job of a net worth statement: one page that answers the only question that compounds. Are you worth more than you were a year ago? Here's how to read one line by line, and how to track yours without turning it into a part-time job.

What is a net worth statement?

A net worth statement (sometimes called a personal balance sheet) is a one-page summary of everything you own (assets), everything you owe (liabilities), and the difference between the two: your net worth. The formula is simply: Assets − Liabilities = Net Worth. It's a snapshot of your financial position at a single point in time.

Businesses have used balance sheets for centuries for a reason: income statements show motion, but the balance sheet shows position. The same logic applies to you. A high earner who spends everything can have a lower net worth than a modest earner who saves and invests. Your salary is nowhere on this statement, and that's precisely the point.

The anatomy: a sample statement, annotated

Here's a realistic net worth statement for a fictional 34-year-old, with the four things to notice marked ① through ④:

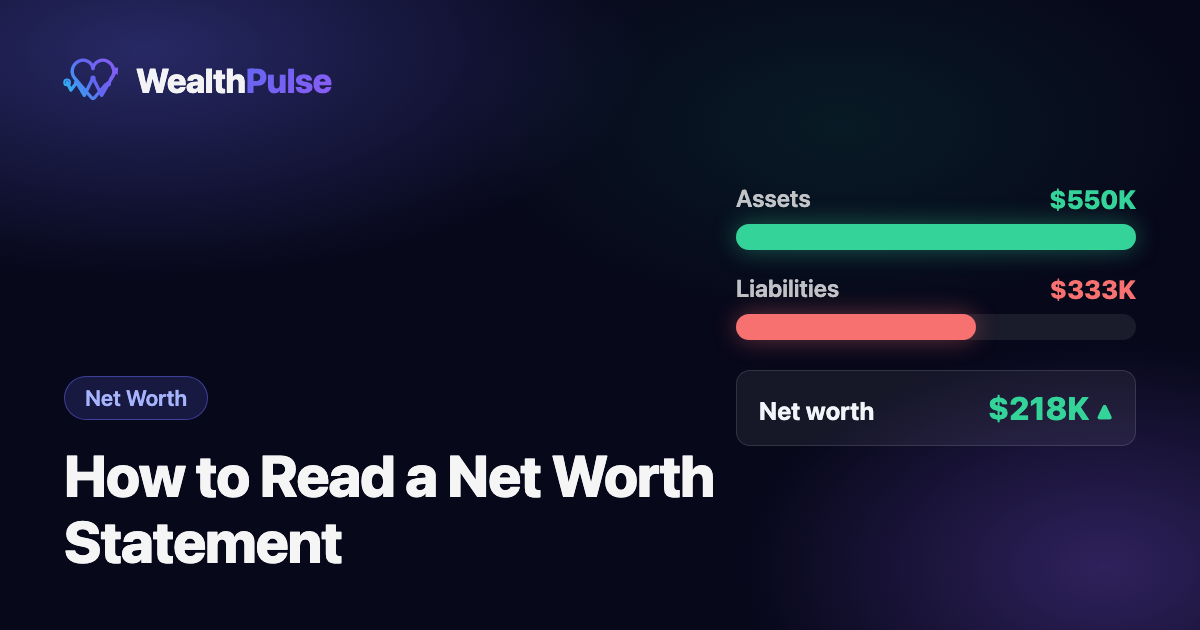

| Checking + savings (liquid) | $18,500 |

| Brokerage account (liquid-ish) | $42,000 |

| 401(k) + Roth IRA (retirement) | $96,000 |

| Home (market value) ② | $380,000 |

| Car (resale value) | $14,000 |

| Total assets | $550,500 |

| Mortgage balance ② | $298,000 |

| Student loans | $22,500 |

| Auto loan | $9,000 |

| Credit card balance ⚠ high interest | $3,200 |

| Total liabilities | $332,700 |

① Assets are grouped by how fast you could touch them. Cash is instant, brokerage takes days, retirement accounts are locked (with penalties) for decades, and a house takes months to sell. Same dollar values, very different usefulness in an emergency. If that retirement line has you wondering whether it's big enough, we've broken down exactly how much you need to retire.

② The house appears twice, and that's correct. The market value sits in assets; the mortgage sits in liabilities. The difference between them ($82,000 here) is your home equity. Listing only one side is the single most common way people get their net worth wrong.

③ Not all liabilities are equal. A mortgage against an appreciating asset is very different from a credit card balance compounding at 20%+. The statement doesn't judge, but you should, and the flag on that credit card line is where a reader's eye should snag first.

④ The bottom line is a snapshot, not a verdict. $217,800 means this person could theoretically sell everything, pay every debt, and walk away with that amount. The comparison to last quarter (up $11,500) is more informative than the number itself.

Reading it like a pro: five signals that matter more than the total

1. Direction beats level. A $40,000 net worth that grew from $25,000 last year is a better story than $400,000 that shrank from $450,000. Track the trend, month over month and especially year over year, since markets make any single month noisy.

2. Liquid net worth is your real safety margin. Strip out the house and retirement accounts and ask what's left. As one wealth manager memorably put it, you can't eat your house. A paper-rich, cash-poor statement still can't handle a $5,000 emergency. If liquid assets are thin, that's your first fix (and where an emergency fund goal belongs).

3. Read the liability mix, not just the sum. Sort your debts by interest rate. Low-rate mortgage debt against an appreciating home builds wealth; double-digit consumer debt destroys it, and it quietly drags on your credit score too. If high-interest balances are growing quarter over quarter, your net worth statement is flashing a warning even if the total is going up.

4. Watch concentration. If one line (usually the house, sometimes one stock) is 80% of your assets, your net worth rises and falls with a single market. The statement makes concentration visible in a way individual account balances never do.

5. Compare against the median, not the average. US average household net worth is roughly $1.06 million, but the median is about $193,000. The average is dragged up by a small number of very wealthy households. If you benchmark at all, benchmark against the median for your age, and remember that negative net worth is completely normal early on: a new graduate with student loans or a fresh homebuyer can be doing everything right while the number sits below zero.

What to leave out

A net worth statement is only useful if it's honest. Leave out future income (it isn't yours yet), unvested stock options or RSUs (same reason), term life insurance (it has no cash value while you're alive), and possessions with negligible resale value. Your furniture and electronics are worth a fraction of what you paid. Use resale values for the car, a realistic estimate for the home, and round conservatively. An inflated statement only lies to its one reader: you.

How to track yours (the 15-minutes-a-month system)

The statement above is a snapshot. The value comes from taking the same snapshot on a schedule and watching the film. Here's the system:

Pick a day and repeat it monthly. First of the month works. Consistency matters more than frequency. Monthly is frequent enough to catch trends and infrequent enough that market wiggles don't dominate.

List every account once, then just update balances. The first session is the slow one: every bank account, brokerage, retirement account, property, and debt. In the WealthPulse Net Worth Tracker, you enter assets and liabilities once and the dashboard maintains a 12-month history chart automatically: the film, not just the snapshot.

Let the pieces feed the whole. Your investment balances move constantly; the Investment Tracker keeps holdings, gain/loss, and allocation current so the asset side of your statement stays honest without manual math. On the other side, the Debt Tracker watches your liabilities shrink, and because it runs your avalanche or snowball plan, every extra payment shows up twice: a smaller liability line today and less interest paid over the life of the debt.

Connect the flow to the position. Your net worth changes for exactly two reasons: what you keep (income minus spending) and what your assets do (growth or loss). The keeping half is your savings rate, which the Budget Planner shows monthly, with the Transaction Log underneath it explaining any month where the number surprised you. If spending has quietly crept, the Subscription Tracker is usually where the leak is hiding.

Give the number a destination. A net worth trend line is motivating; a target makes it strategic. Set milestones (first positive net worth, first $100K, a down payment) in Goals and let the progress rings do the nagging for you.

One number, two very different stories

Why read the whole statement instead of just the bottom line? Because the same net worth can describe two completely different financial lives:

Household A can weather a job loss, jump on an opportunity, and rebalance at will. Household B is wealthy on paper and fragile in practice. Nothing about the bottom line reveals that. Only reading the statement does.

The bottom line

A net worth statement is the rare financial document that fits on one page and still tells the truth: what you own, what you owe, and which direction you're heading. Read it for the trend, the liquidity, the debt mix, and the concentration, not for a verdict on your worth. Then automate the tracking so the snapshot becomes a film. Fifteen minutes a month, and the most important number in your financial life stops being a mystery.

Your net worth, updated automatically. WealthPulse tracks your assets, liabilities, and 12-month net worth history alongside your budget, debts, and goals. The whole statement, one dashboard, always current.

Start your free 7-day trial →Frequently asked questions

What is a net worth statement?

A net worth statement, sometimes called a personal balance sheet, is a one-page summary of everything you own (assets), everything you owe (liabilities), and the difference between them (your net worth). It's a snapshot of your financial position at a single point in time.

How do I calculate my net worth?

Add up the current value of everything you own (cash, investment and retirement accounts, home value, vehicles), then subtract everything you owe, including your mortgage, auto and student loans, and credit card balances. Assets minus liabilities equals net worth.

What should you not include in a net worth statement?

Leave out future income, unvested stock options, term life insurance, and possessions with little resale value. These don't reflect what you could actually access today, so including them inflates the picture.

Is it bad to have a negative net worth?

Not necessarily. Negative net worth is common early in a career or right after buying a home, when student loans or a fresh mortgage outweigh assets. What matters is the direction: if liabilities are falling and productive assets are growing, you're on the right track even while the number is below zero.

What is the average net worth in the US?

Per the Federal Reserve's Survey of Consumer Finances, the average US household net worth is roughly $1.06 million, but the median is about $193,000. The average is pulled up by a small number of very wealthy households, so the median is the more realistic benchmark for a typical household.

How often should I update my net worth statement?

Monthly is the sweet spot for most people: frequent enough to catch the trend, infrequent enough that market noise doesn't dominate. Update account balances, refresh your home's estimated value quarterly or so, and compare against last month and last year rather than day to day.

This article is general educational information, not financial advice. All analysis is for informational purposes only. Benchmark figures come from the Federal Reserve's Survey of Consumer Finances and are subject to revision. For guidance specific to your situation, consider speaking with a qualified financial professional.

Take control of your money

Budgeting, investing, and AI analysis in one dashboard. 7-day free trial.

Start free trial →